UK Energy Market Report — April & May 2026

16/06/26

Market Overview

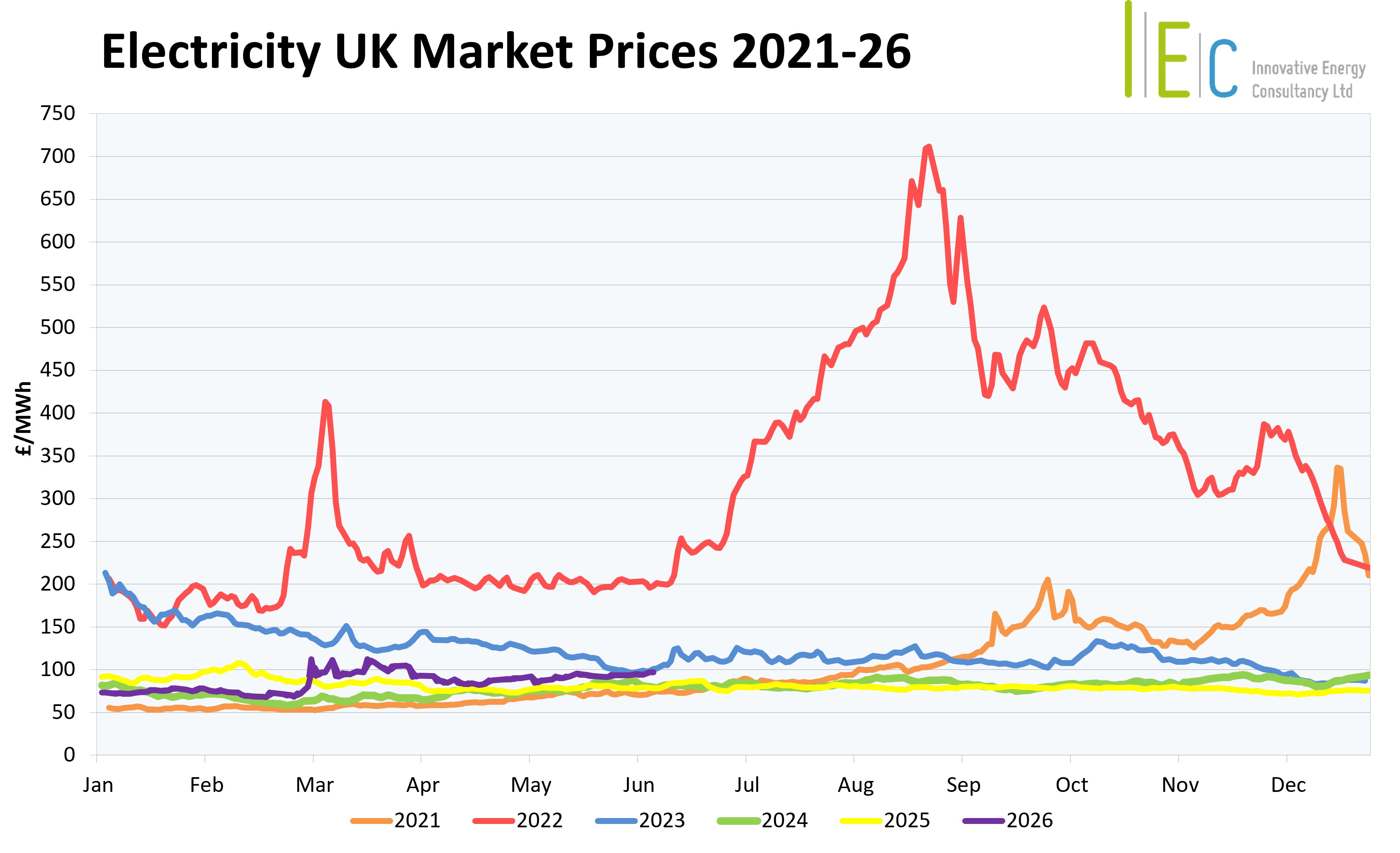

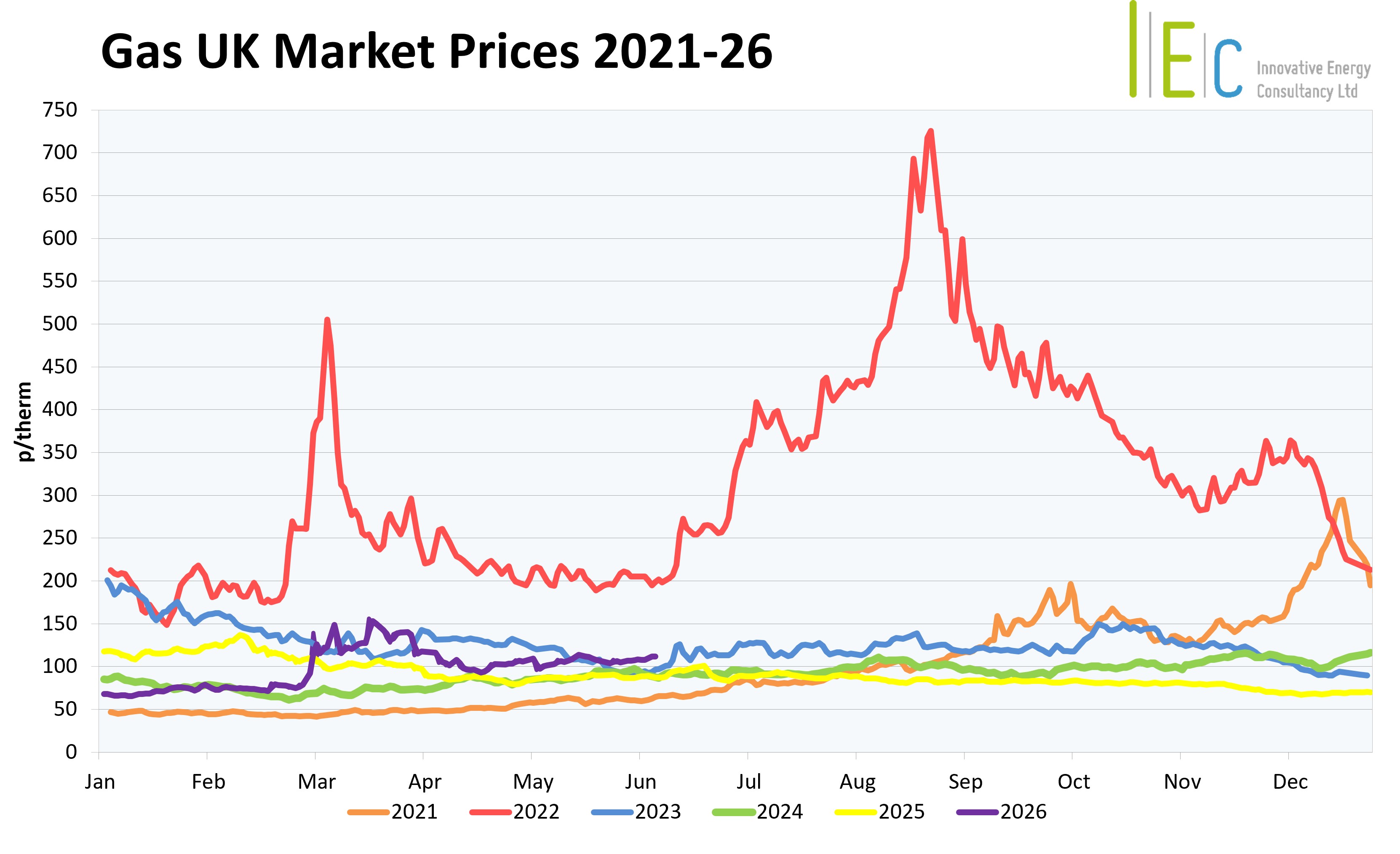

The UK energy market across April and May 2026 was driven by sustained geopolitical disruption and tightening gas fundamentals, with a clear evolution in both gas and power dynamics.

In April, markets were highly reactive, with sharp price swings driven by US–Iran ceasefire developments and uncertainty around the Strait of Hormuz. While gas prices remained volatile, gas demand for power generation was reduced, thanks to strong wind and renewable generation, limiting the impact of hydrocarbon price spikes into the electricity markets.

By May, the market shifted into a more structurally tight phase. In gas, low European storage levels, constrained LNG supply, and continued disruption to Hormuz flows embedded a persistent risk premium. In power, weaker wind output and lower nuclear availability increased reliance on gas-fired generation and imports, tightening system conditions.

This marked a transition from a predominantly event-driven market in April to one in May where both gas fundamentals and power system constraints played a sustained role in supporting prices and volatility.

Supply & Storage Conditions

European gas supply remained constrained throughout both months due to the sustained disruption of LNG flows through the Strait of Hormuz. In April, supply conditions fluctuated in line with ceasefire developments, with prices falling sharply following a temporary truce but recovering as negotiations repeatedly broke down and blockades persisted. LNG shipping remained minimal, limiting any meaningful supply response and keeping the market sensitive to headlines.

In May, supply tightness became more entrenched, with the Strait still largely closed and global LNG flows structurally reduced. European storage levels increased only modestly, reaching around 39% by month-end, well below seasonal norms and highlighting the challenge of refilling inventories. Additional pressure came from reduced Norwegian flows due to maintenance and rising Asian demand, which intensified competition for limited cargoes. As a result, supply dynamics shifted from short-term disruption in April to sustained scarcity in May.

Demand Drivers

Demand played a secondary but evolving role across the period, initially providing some relief before contributing to tightening conditions. In April, relatively soft demand and strong renewable output reduced reliance on gas-fired generation, supporting weaker prices during periods of geopolitical easing. This contributed to a more balanced system, despite underlying supply risks.

In May, demand dynamics became more supportive, driven primarily by the start of Europe’s storage injection season. The need to rebuild inventories, particularly from below-average levels, added consistent structural demand into an already constrained system. At the same time, increased LNG demand from Asia, linked to seasonal cooling needs, tightened the global balance further. While real-time consumption remained relatively stable, these structural factors shifted demand conditions from neutral in April to increasingly supportive of higher prices in May

Geopolitical Considerations

Geopolitical developments were the dominant driver of market movements, with the US–Iran conflict directly impacting global LNG supply.

In April, markets reacted sharply to each development, with ceasefire announcements triggering steep price declines and renewed tensions causing rapid rebounds. The repeated failure of negotiations, combined with the continued blockade of the Strait of Hormuz, kept markets highly unstable.

By May, the conflict had evolved into a prolonged stalemate, embedding a sustained risk premium into energy prices. Reduced LNG availability forced Europe into greater competition with Asian buyers, while infrastructure risks in the Gulf highlighted supply fragility. Alongside this, reduced Russian gas flows and ongoing sanctions continued to underpin tight European market conditions, amplifying sensitivity to LNG disruptions.

Power Generation Mix (UK)

The UK generation mix shifted materially from April to May, with reduced renewable contribution and higher reliance on thermal generation and imports.

In April, strong wind output dominated at 31%, enabling gas to fall to 16% and supporting a relatively balanced, lower-carbon system. Nuclear and imports each contributed 16% and 15% respectively, while solar reached 11% and biomass remained stable at 7%, reinforcing reduced dependence on marginal gas.

In May, weaker wind conditions drove a rebalancing of the system towards more price-sensitive sources. Wind fell to 25%, while gas increased to 23%, highlighting greater reliance on thermal generation. Imports rose to 19%, indicating tighter domestic supply and increased interconnector dependence, while nuclear declined to 11%, reducing baseload stability. Solar edged up to 12% and biomass remained unchanged at 7%.

Overall, the May mix increased exposure to gas pricing, reinforcing its role as the marginal driver of power prices. Following the sharp decline in the UK’s carbon price at the start of 2026, it has now recovered to reach 2025’s average levels of £56 per tonne by end of May.

We meet all your

business energy needs

Find out how much money

we’ve saved for our clients,

or to arrange an informal

discussion with one of

our energy experts,

please call 01244 571830