February 2026 UK Energy Market Drivers

11/03/26

Market overview

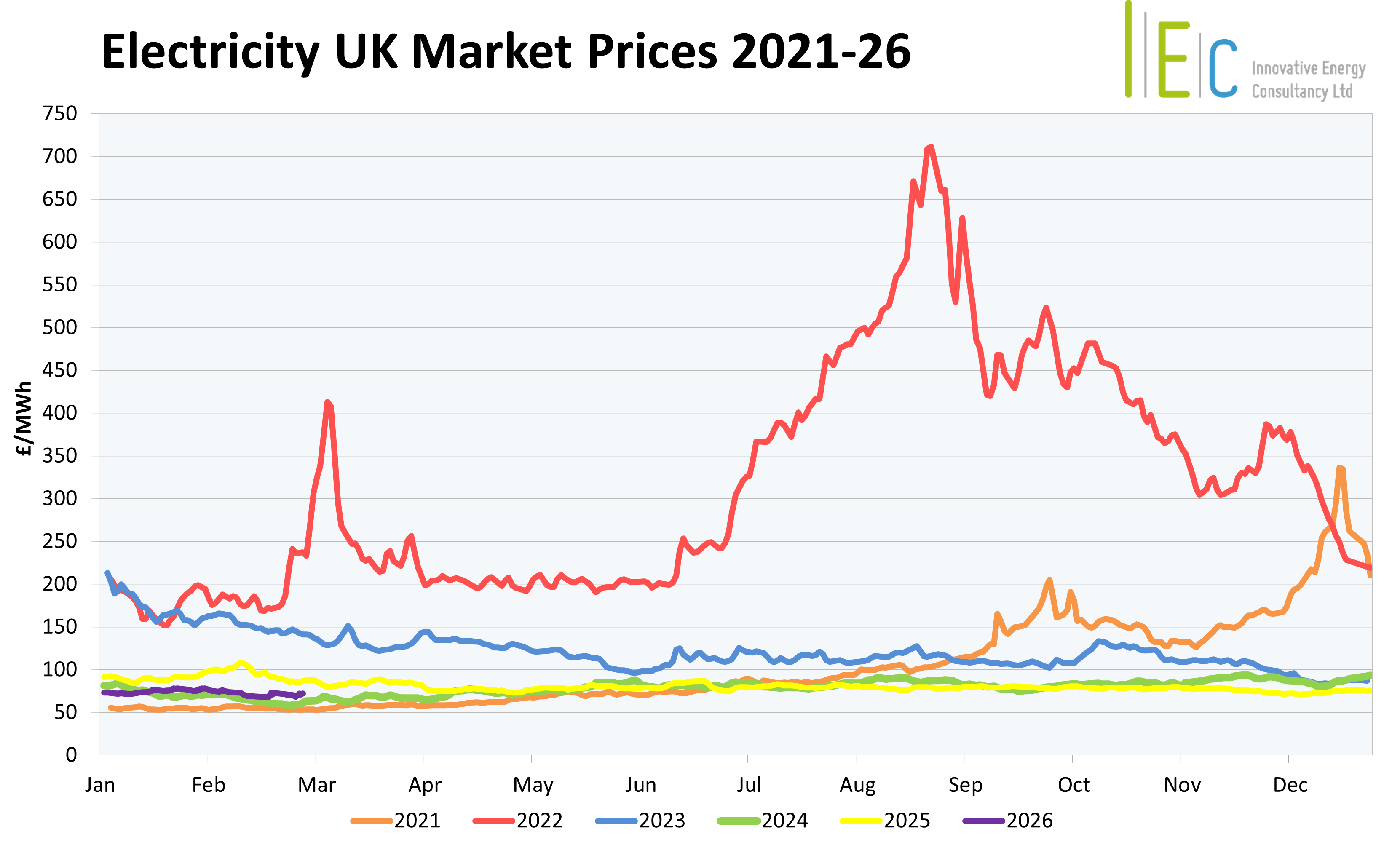

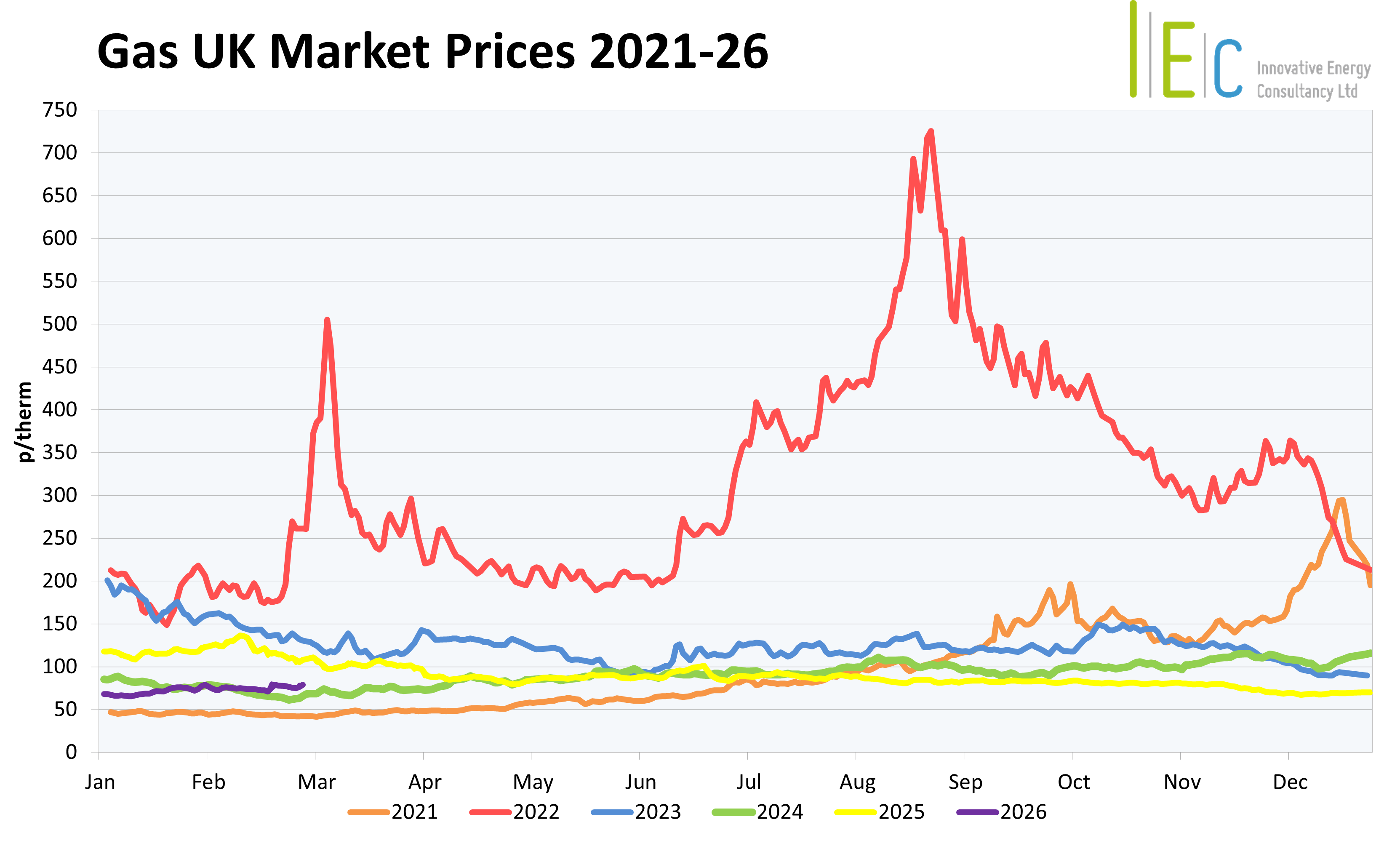

February 2026 can be characterised as a month in which strong renewable generation, milder temperatures, and steady LNG inflows helped offset the risks posed by low European storage. Gas demand in the UK was moderated by elevated wind output and softened heating requirements, while supply remained heavily dependent on domestic and Norwegian flows, supplemented by increased LNG. Yet despite these stabilising factors, geopolitical uncertainty and tight storage conditions continued to exert upward pressure during certain trading sessions.

Supply and storage conditions

European storage remained structurally tight throughout February, with levels fluctuating between 30% and 41%, leaving the continent vulnerable to any late season cold spells. Milder weather reduced withdrawals, while LNG arrivals helped stabilise fundamentals mid-month. In February, 58% of GB gas supply originated from UK and Norwegian fields, 35% came from LNG imports, and 7% from storage withdrawals, with minimal imports via European pipelines. This aligns with broader European patterns of constrained storage and increased dependence on flexible LNG.

Demand drivers

Gas demand tracked the weather closely. Persistent expectations of above seasonal temperatures reduced heating requirements, easing pressure on both storage withdrawals and spot market pricing. Occasional cold spell risks – including signals of potential stratospheric warming – triggered temporary upward price movements, but these episodes were short lived and outweighed by the broader mild trend.

Geopolitical considerations

Geopolitical risks remained an important amplifier of volatility. Concerns over potential US military action in Iran intermittently lifted prices, as traders assessed the risk of disruption to LNG carriers transiting the Strait of Hormuz. These geopolitical episodes repeatedly injected risk premium into prices before fading as diplomatic signals stabilised.

Power generation mix (UK)

There were notable swings between wind and gas fired generation throughout February, with wind output strengthening on several days and easing reliance on CCGT, while lower wind intervals raised gas fired generation. UK generation data reveals that wind was the single largest source of electricity in February, delivering 36.3% of total generation. Gas fired power contributed 29.4%, followed by nuclear at 10.5%, biomass at 6.7%, solar at 2.3%, and imports at 11.9%, with hydro and storage providing marginal shares. Following the sharp rise in the UK’s carbon price at the end of 2025, the gains have now reversed seeing an equally steep fall since mid-January. The drop has been caused by the market being saturated with surplus allowances, weakened confidence in government plus mild weather reducing energy demand, leading to the UK ETS trading at a heavily discounted price of £46 per tonne by end of February.

We meet all your

business energy needs

Find out how much money

we’ve saved for our clients,

or to arrange an informal

discussion with one of

our energy experts,

please call 01244 571830