UK Gas & Electricity Market Overview – April 2025

15/05/25

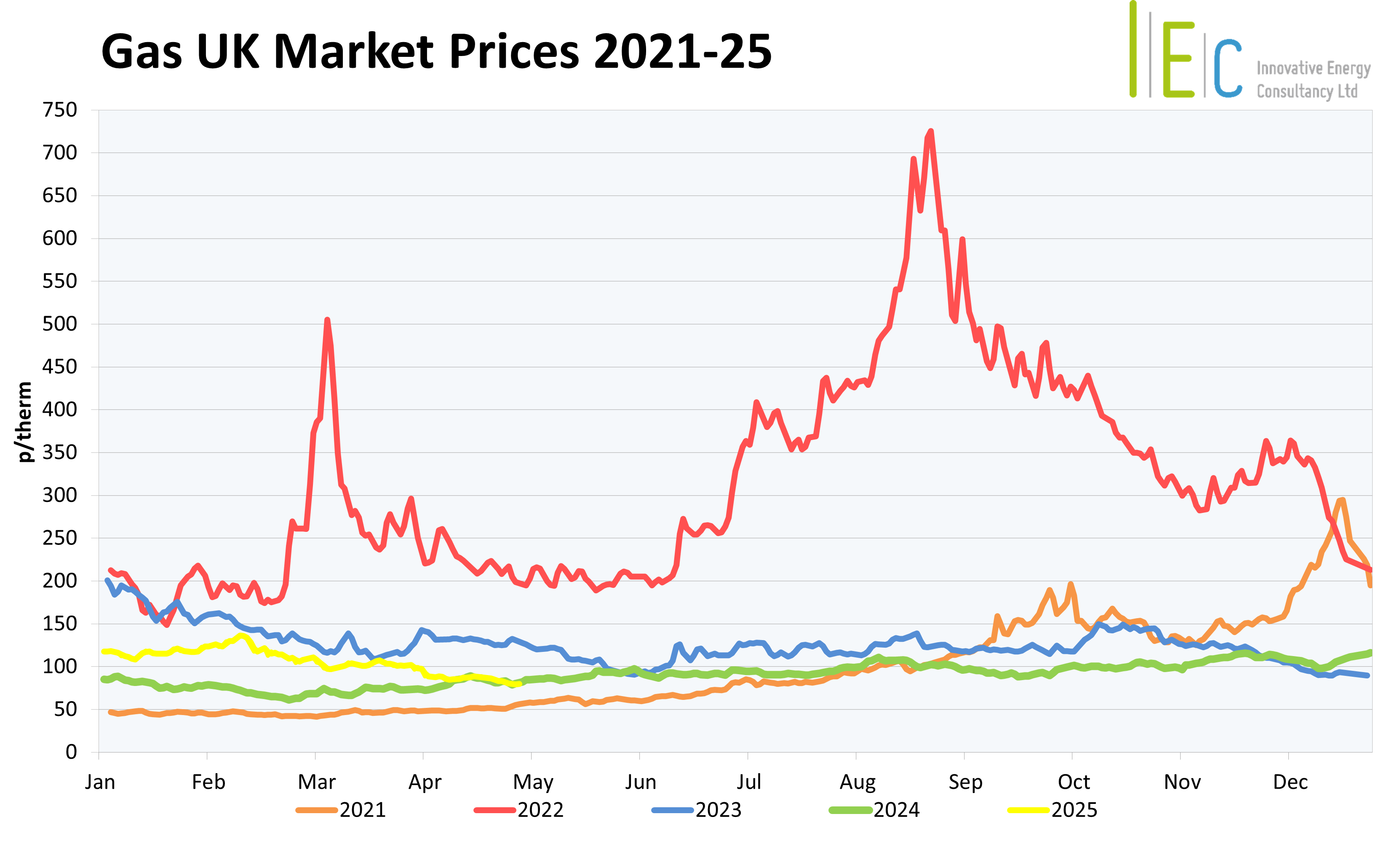

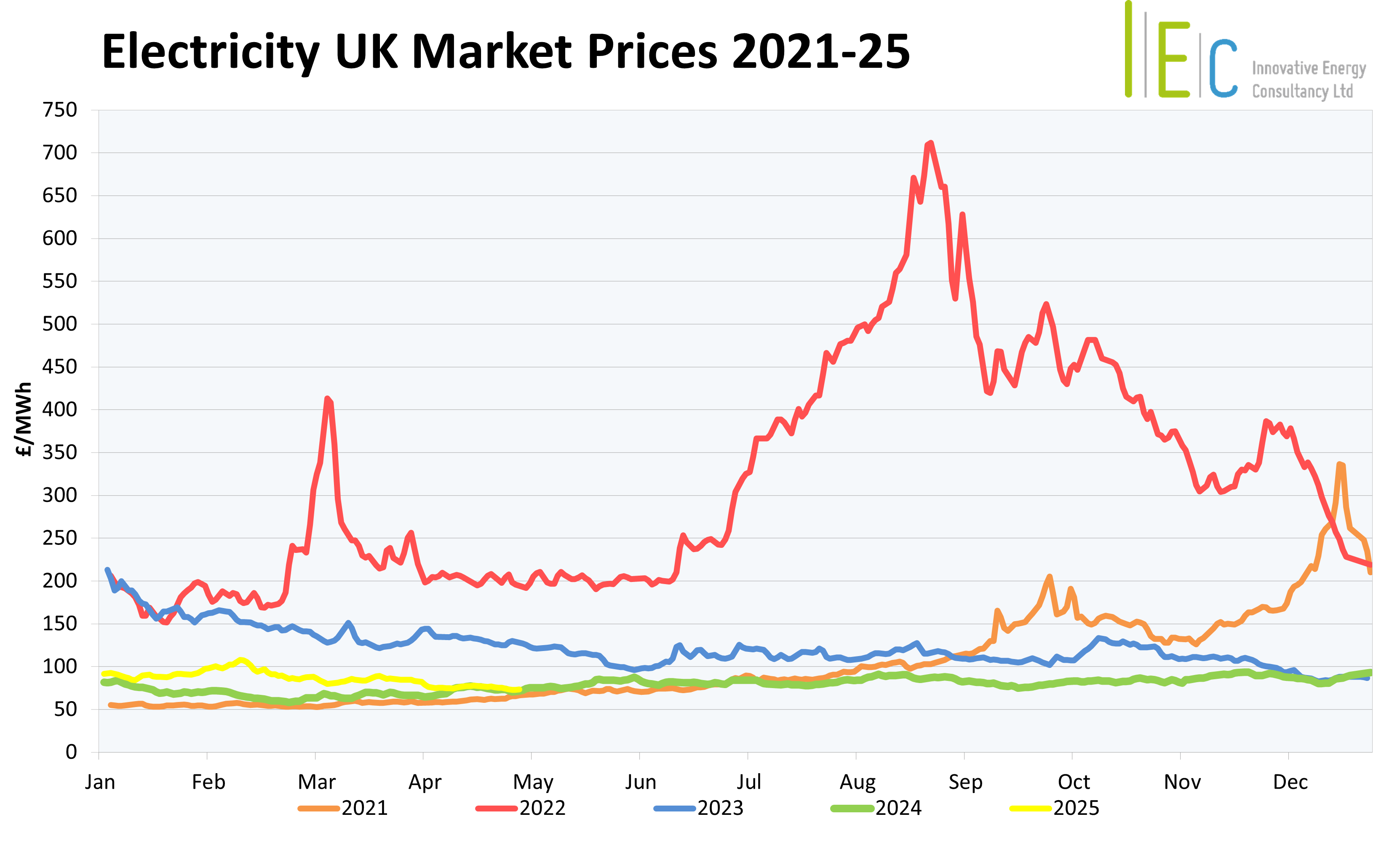

April 2025 was a dynamic month for UK energy markets, with bullish and bearish pressures alternating due to a mix of supply constraints, demand shifts and geopolitical uncertainty. EU storage levels and Norwegian gas disruptions created bullish conditions, while Trump’s tariffs and strong renewable output exerted bearish pressure. LNG remained the key balancing factor, with global trade conflicts and weather forecasts shaping price movements. As Europe moves into the summer months, competition for LNG, storage injection rates and geopolitical developments will continue to drive market volatility.

Supply Factors – EU Storage Levels, LNG Imports and Global Supply Disruptions

One of the most significant drivers on UK energy markets was EU gas storage levels, which ended March at just 34% full, compared to 58% last year. This created sustained bullish pressure on gas prices as Europe sought to replenish inventories before winter. LNG remained a key balancing factor, with Europe competing for cargoes amid fluctuating Asian demand. While weaker LNG imports into Asia allowed Europe to stockpile at favourable prices, disruptions in Malaysia, Australia, and Brunei introduced some uncertainty into the supply chain. Additionally, the trade battle between US and China led to more LNG cargoes being redirected to Europe. This mitigated some supply concerns, allowing Europe to begin rebuilding storage levels, while maintaining adequate supply for electricity production. Norwegian gas flows were disrupted mid-month due to maintenance outages and processing challenges at key facilities, including the Aasta Hansteen gas plant. These disruptions tightened supply conditions, contributing to upwards price movements. By late April, Norwegian flows had returned above the five-day moving average, helping to stabilise the market.

Demand Factors – Weather Patterns, Seasonal Demand and Renewable Energy Output

Northern European gas demand was heavily influenced by weather forecasts, with predictions of a hot summer increasing competition for LNG, as cooling demand rose. This bullish factor was particularly relevant in mid-to-late April, as traders anticipated stronger demand from Asia, which could divert LNG cargo away from Europe. Conversely, colder spells early in the month drove short-term price spikes, as heating demand surged across the EU.

The role of renewable energy in shaping market conditions was also evident throughout April. Intermittent periods of increased wind and solar generation helped reduce reliance on gas-fired power, exerting bearish pressure on prices.

Geopolitical Factors – Trump Tariffs and Trade Uncertainty

Trump’s newly imposed tariffs weighed on global economic activity and subsequently energy demand, leading to bearish price movements early in the month. The tariffs, which targeted exports from multiple nations, raised concerns about a global economic slowdown, reducing industrial energy consumption. However, a temporary postponement of certain tariff measures provided brief relief, allowing prices to recover.

Trade tensions between US and China continued to influence LNG flows. Weaker Asian demand, driven by China’s reduced LNG imports (down 20% year-over-year), allowed Europe to stockpile at lower prices. However, caution remains as any policy shifts or economic recovery in Asia could reverse this trend, tightening supply and pushing prices higher.

Power Generation

April 2025 saw the UK continue its reliance on gas for power generation, providing 26% of the power mix. The month saw an extended period of favourable weather, which provided strong solar generation (11%). However, this was not enough to supplement the reduced wind strength and subsequent drop in on and off-shore generation (22% – its second lowest April in five years). Nuclear generation also continued on a downward trend (14%), placing additional pressure on the grid to find other sources to compensate, with it ultimately arriving from the continent (18% – highest April in five years), reflecting an increasing reliance on cross-border supply, to maintain grid stability. The UK’s Emissions Trading Scheme (UKETS) again saw a month-on-month climb of 10%, closing April at £48/tonne.

We meet all your

business energy needs

Find out how much money

we’ve saved for our clients,

or to arrange an informal

discussion with one of

our energy experts,

please call 01244 571830