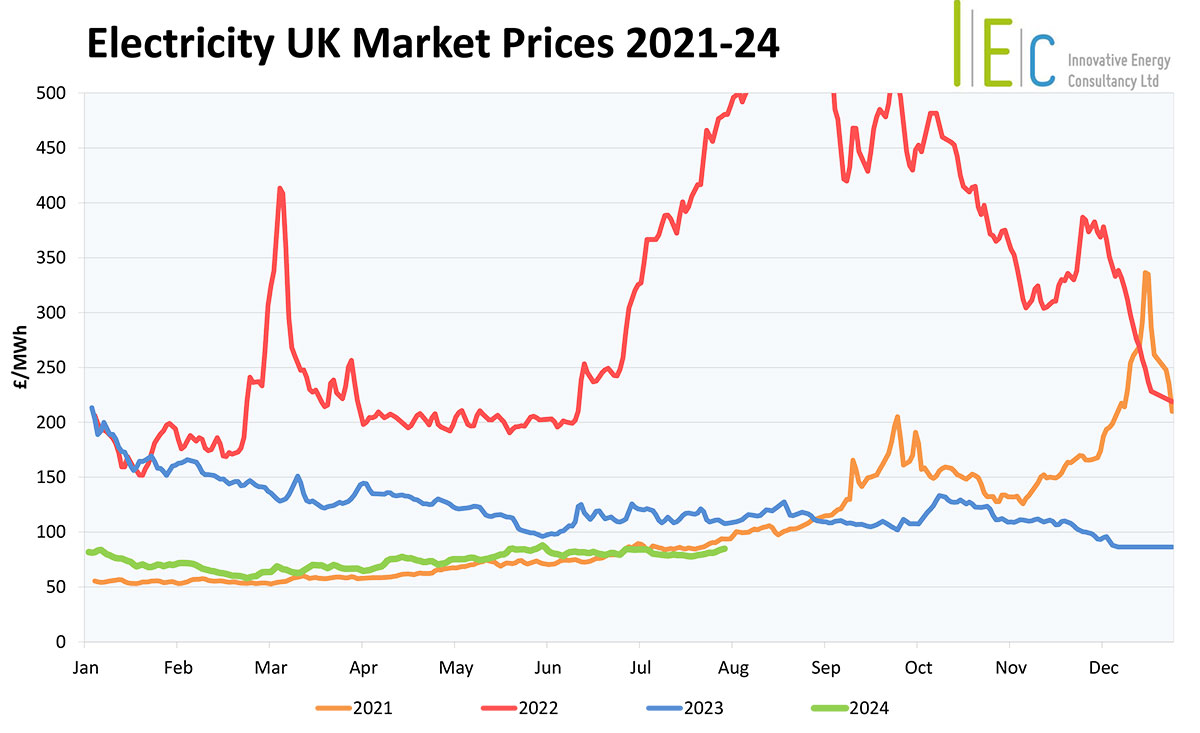

UK Gas and Electricity Market Overview: May – July 2024

11/09/24

After a rise through May, the markets remained supportive but stable across June and July. Despite brief periods of above average temperatures, the UK’s summer 2024 has been milder than historical averages, reducing energy demands for cooling requirements. The UK and European supply has, as expected, been mixed, due to the ongoing maintenance season. However, globally there have been a few shock interruptions, which have put short-term pressures on the markets.

Strong gas storage levels

European gas storage remains in a position of strength, increasing to 84% by mid-July, above the five-year average and level with 2023. Mild temperatures and limited supply issues have reduced withdrawal requirements and enabled a steady increase of injections across the summer. Forecasts expect EU storage levels to reach 90% by the autumn. This positive outlook continues to be the major bearish force on the markets, helping to provide stability against outbreaks of short-term bullish influences.

Pressure on LGN supplies

Geopolitical issues and extreme weather have caused major delays to international shipping, with many liquified natural gas (LNG) cargoes forced into detours or left anchored, adding pressure to global LNG supplies. Deliveries to Europe have reduced further, due to increasing competition from Asia following disruption at Australia’s Wheatstone gas facility and an extended heatwave, causing them to look west for supplies. A new package of EU sanctions on Russian gas was introduced focusing on restricting its LNG imports. Despite these factors, European LNG demand has been stable and so the price rates have only increased moderately. Analysts predict that by 2030, there will be an 11% oversupply of LNG in the world, due to a number of new projects that will surpass the rate of growth in demand.

Limited demand spikes

The UK power mix has been balanced across the summer, with gas providing the majority at an average of 36%. Renewable generation has fluctuated, with the milder weather hindering both wind and solar power generation and only representing around 25% of the summer mix. However, the milder weather has also limited any demand spikes for additional cooling requirements, helping to maintain a balanced system and easing any bullish pressures. UK Emissions Trading Scheme (UKETS) price rallied to a peak of £50/tonne mid-June before lowering back to £40/tonne by the time of writing.

We meet all your

business energy needs

Find out how much money

we’ve saved for our clients,

or to arrange an informal

discussion with one of

our energy experts,

please call 01244 571830