UK Energy Market Movements - July 2025

27/08/25

Throughout July 2025, the UK energy market experienced a blend of moderate volatility and strategic adjustments, shaped by a combination of supply constraints, rising demand, geopolitical developments, and shifts in power generation.

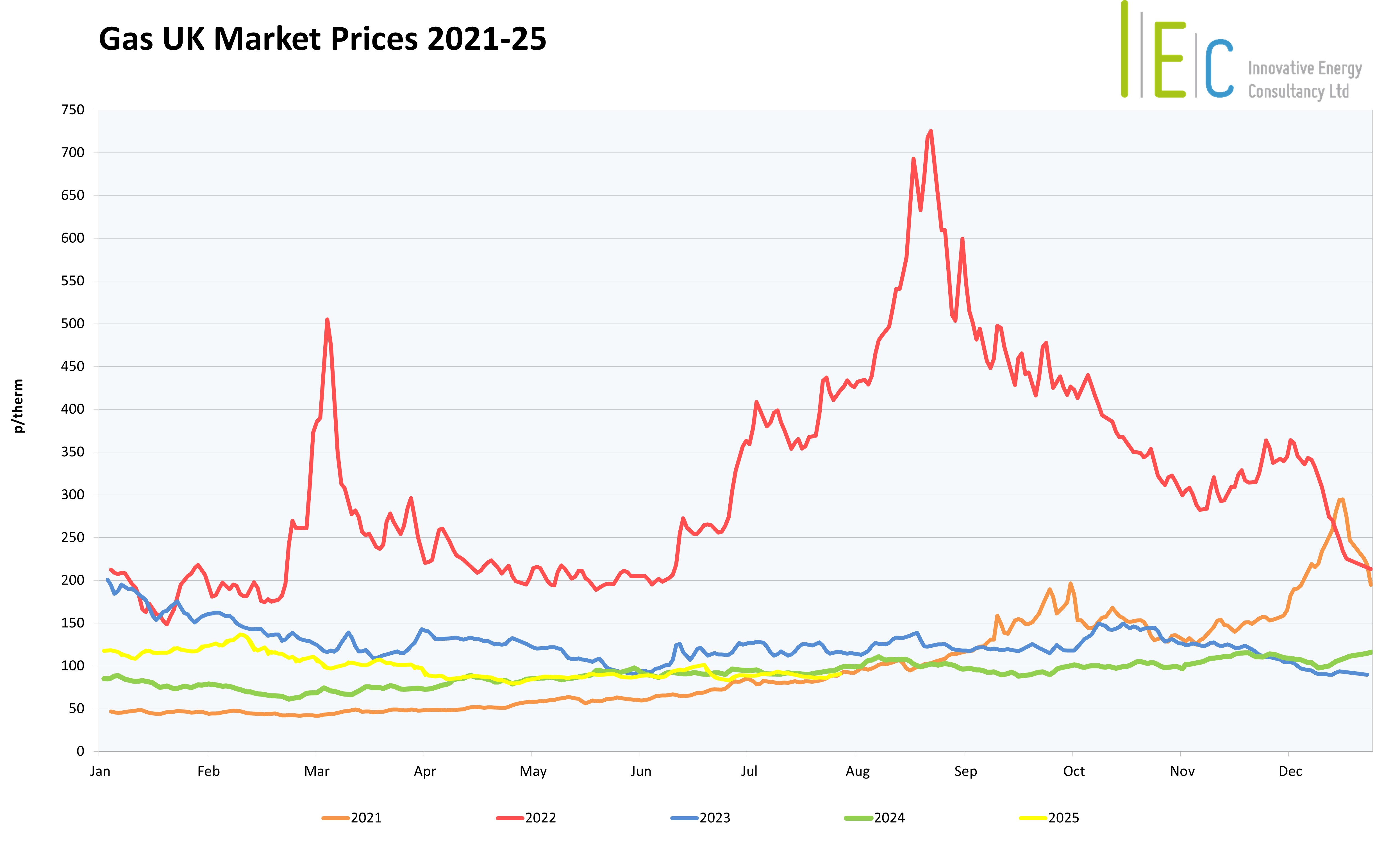

Gas prices showed a slight upward trend overall, with the average daily change recorded at +0.00389. Despite intermittent disruptions, EU gas storage levels increased from 59% to 68%, reflecting a concerted effort to prepare for the upcoming winter season. These movements were influenced by both domestic factors and broader international dynamics.

Supply Factors

Supply conditions in the UK were notably tight during July, with the gas grid most frequently operating under-supplied. This was largely due to disruptions in Norwegian gas flows, particularly from the Nyhamna and Kollsnes processing facilities, which experienced outages linked to power supply issues. Although these outages were temporary, they underscored the fragility of Europe’s energy supply chain. Nevertheless, strong LNG imports and piped gas flows helped the EU steadily build its reserves, resulting in a 9% increase in storage levels to reaching 68% at the month’s close. The market remained sensitive to any supply-side developments, especially those affecting key infrastructure.

Demand Factors

Demand pressures were elevated throughout the month, driven primarily by extreme weather conditions. Heatwaves across Europe and Asia significantly increased the need for cooling, which in turn boosted energy consumption. China’s LNG imports surged to a yearly high, while Japan and Southern Europe also faced above-average temperatures, intensifying competition for fuel.

These conditions placed additional strain on the market, as traders sought to balance immediate demand with long-term storage goals. The seasonal spike in energy usage highlighted the importance of maintaining robust supply channels and flexible import strategies.

Geopolitical Factors

Geopolitical developments played a central role in shaping market sentiment and price movements.

US President Donald Trump’s evolving trade and sanction policies introduced considerable uncertainty. His threats to impose tariffs on Russia, and secondary sanctions on China and India, created concerns about potential disruptions to global energy flows. However, progress in trade negotiations between the US and EU later in the month helped stabilize the market and improve investor confidence. The ongoing conflict in Ukraine remained a persistent backdrop, influencing strategic decisions and contributing to overall market volatility.

Power Generation Factors

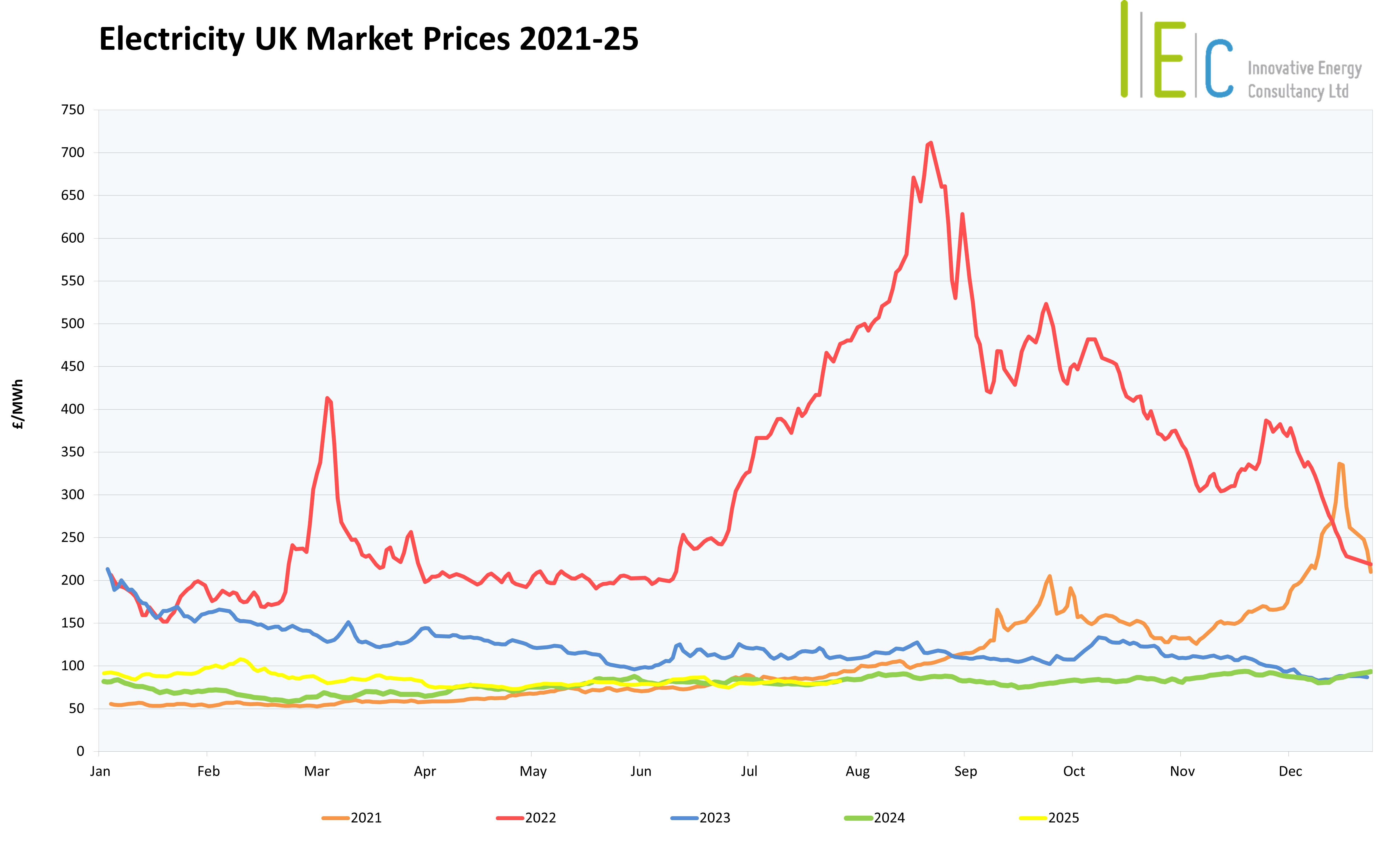

The UK’s power generation mix reflected a balanced but weather-sensitive approach. Gas-fired generation (CCGT) accounted for an average of 13.8% of the total mix, while wind power contributed a more substantial 23.4%. Wind generation varied in response to changing weather patterns, whereas CCGT remained relatively stable.

Elsewhere in Europe, nuclear output was affected by rising river temperatures, particularly in France, which had indirect implications for UK energy dynamics. These shifts in generation sources underscored the importance of diversification and adaptability in the face of environmental and geopolitical challenges. Following on from a sharp drop in June, the UK’s Emissions Trading Scheme (UKETS) price rebounded to reach £52/tonne by July’s close.

We meet all your

business energy needs

Find out how much money

we’ve saved for our clients,

or to arrange an informal

discussion with one of

our energy experts,

please call 01244 571830