UK Energy Market Movements – August 2025

12/09/25

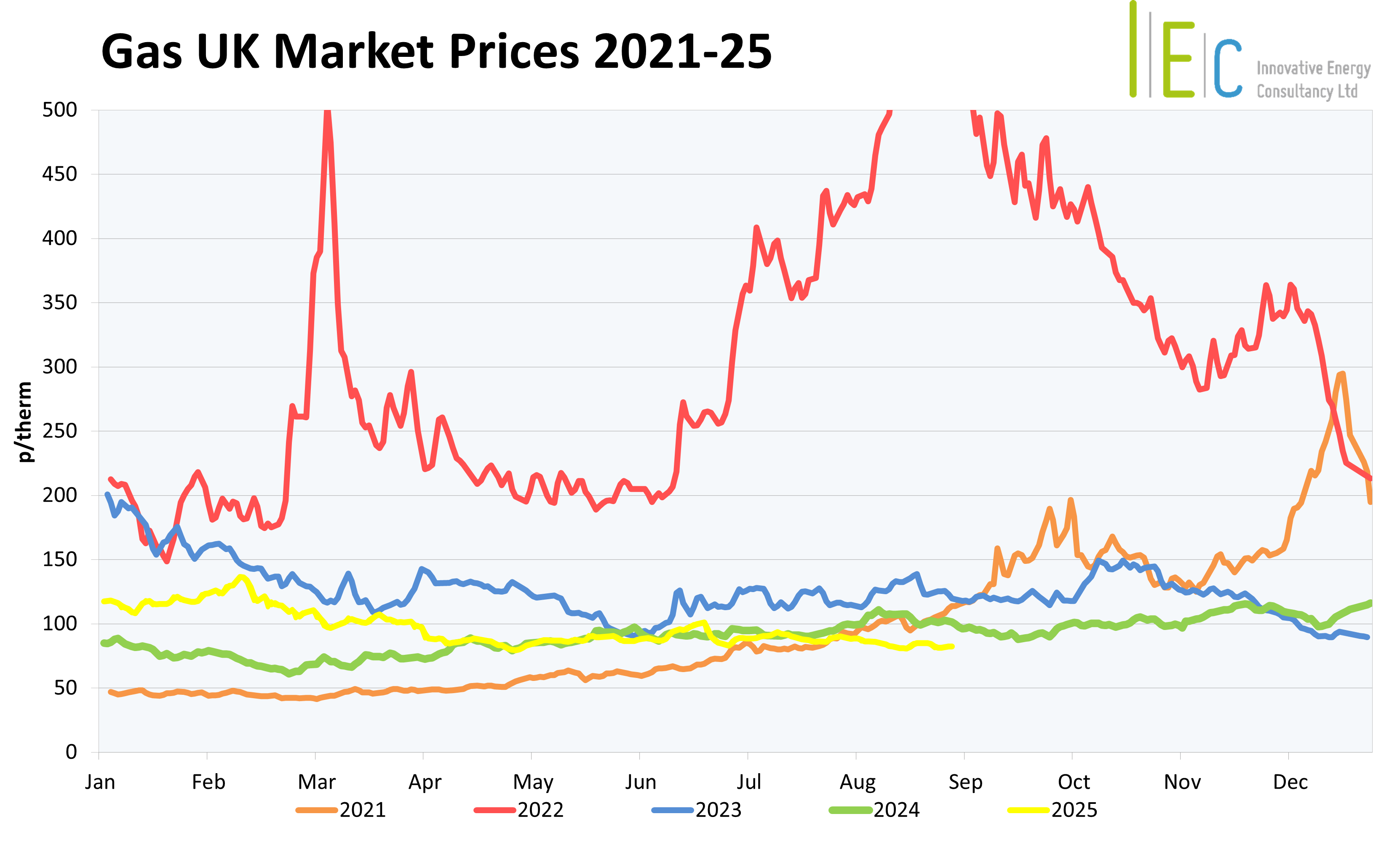

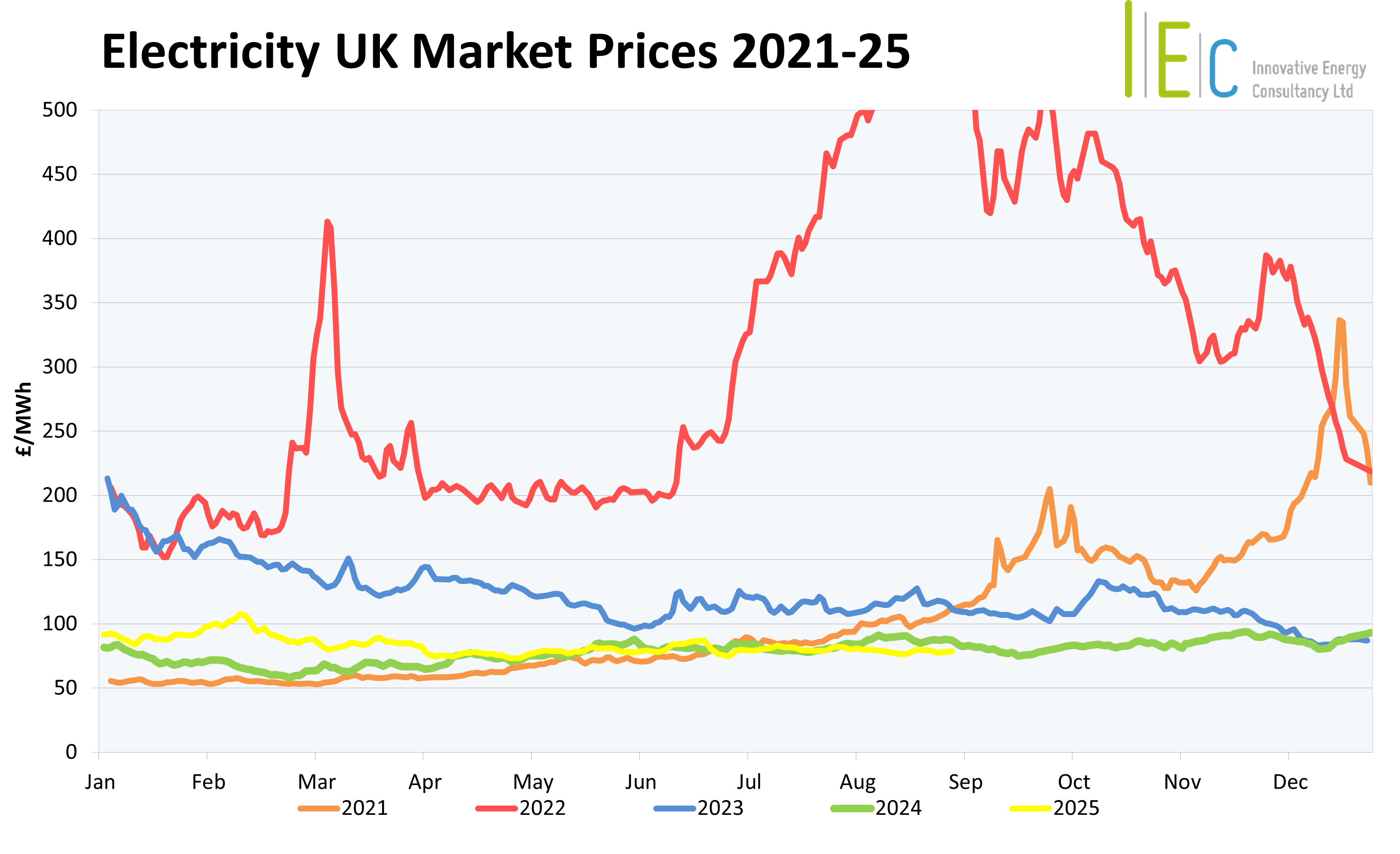

In August 2025, the UK energy market was shaped by a convergence of geopolitical uncertainty, seasonal demand pressures and fluctuating supply conditions. Gas prices trended downward overall, with several days hitting new lows for the year. EU gas storage level continued a steady rise to 77%, reflecting strong efforts to prepare for the winter heating season. As with recent months, the market remained sensitive to developments in the Russia–Ukraine conflict, as well as to diplomatic manoeuvres by the United States. Meanwhile, weather patterns across Europe played a significant role in moderating demand, with intermittent heatwaves driving short-term spikes in cooling needs.

Supply Factors

August saw a generally favourable supply environment for the UK and wider European gas markets, though not without moments of tension. After a strong start, Norwegian gas flows remained relatively stable throughout the month, despite intermittent maintenance at key facilities like the Troll field, which had been flagged earlier in the summer as a potential risk to supply continuity. On the occasional days when Norwegian flows dipped below the five-day moving average, the availability of alternative sources, including liquefied natural gas (LNG) imports and strong wind power generation, helped to soften the impact. EU gas storage levels rose steadily throughout the month, climbing from 68% to 77%. This progress was crucial, given the narrowing window before the winter heating season begins. Traders remained focused on ensuring sufficient injections, and the market responded positively to signs that Europe was on track to meet its storage targets — even amid geopolitical uncertainty and global competition for LNG.

Demand Factors

Demand dynamics in August were shaped by a tug-of-war between seasonal weather patterns and broader macroeconomic forces. While parts of Europe experienced heatwaves in northwest regions, other areas saw milder, overcast conditions that helped ease the pressure on cooling demand. This variability in temperature created short-term fluctuations in gas consumption, with traders responding quickly to updated forecasts. Global competition for LNG remained intense. China’s relatively subdued demand early in the month allowed Europe to accelerate its storage injections, but traders remained cautious, knowing that any uptick in Asian consumption could quickly tighten the market. The underlying demand narrative was one of strategic accumulation rather than reactive consumption. With the winter heating season approaching, European buyers focused on securing volumes whilst market conditions remained favourable.

Geopolitical Factors

Geopolitical tensions remained a dominant force in shaping the UK energy markets. The ongoing conflict in Ukraine continues to cast a long shadow over European energy strategy, with Russian military strikes on Ukrainian infrastructure raising fresh concerns about supply security. US President Donald Trump’s diplomatic manoeuvres added further complexity. His repeated ultimatums to Russia, threats of sanctions and calls for peace negotiations with Ukraine created waves of speculation in the market. While some traders hoped for a breakthrough that might ease restrictions on Russian energy exports, others remained sceptical, noting that even a ceasefire would not guarantee the return of pipeline gas to Europe. The broader geopolitical landscape also included trade negotiations with China, which influenced global LNG flows. Overall, the backdrop of geopolitics in August was one of cautious optimism tempered by the reality of entrenched conflicts and long-term strategic shifts.

Power Generation Factors

The UK’s power generation mix in August reflected a steady reliance on both renewable sources and gas-fired, with notable shifts driven by weather conditions. Wind power was the largest source for August, though mid-month heatwaves brought periods of high pressure and reduced windspeeds, placing greater pressure on gas-fired plants to meet short-term needs. Both provided 26% and 23% of overall power generation, respectively, balancing to maintain grid stability during periods of fluctuating demand. Elsewhere in Europe, nuclear generation faced challenges due to environmental constraints, including elevated river temperatures affecting cooling systems and a jellyfish infestation! These disruptions had an indirect effect on UK market sentiment, as a strong reliance on imports (20%) reinforced the importance of maintaining a diversified generation portfolio capable of adapting to both seasonal and geopolitical pressures. The UK’s Emissions Trading Scheme (UKETS) price had a slight gain through August, reaching £54/tonne at the month’s close.

We meet all your

business energy needs

Find out how much money

we’ve saved for our clients,

or to arrange an informal

discussion with one of

our energy experts,

please call 01244 571830