January 2026 UK Energy Market Drivers

16/02/26

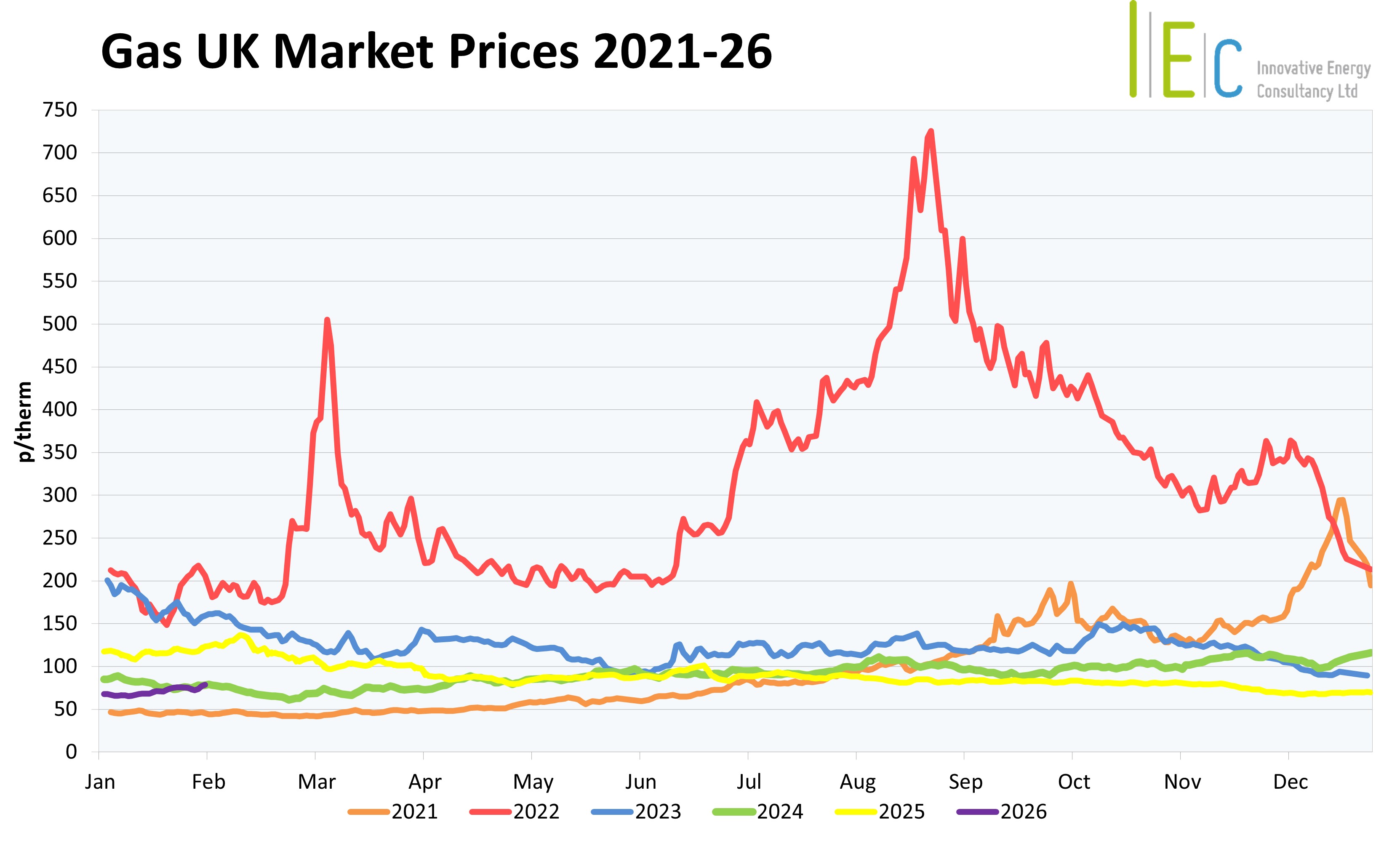

January 2026 was defined by significant volatility across the UK energy market, driven largely by erratic weather patterns, tightening gas fundamentals and persistent geopolitical uncertainty. Market sentiment shifted almost daily as temperature forecasts oscillated between prolonged cold spells and periods of milder-than-expected conditions, producing sharp fluctuations in both gas prices and demand expectations. The month began with forward?month contracts softening as longer?term models predicted a move back towards seasonal norms, only for subsequent cold spells to reverse the trend repeatedly throughout the month. Compounding these dynamics was a steady decline in EU gas storage, which started around 61% on 5 January and fell progressively to approximately 46% by the end of the month, keeping European and UK markets structurally tight and highly sensitive to any disruptions.

Supply Factors

Supply-side conditions remained fragile from the outset. Additional LNG cargoes began heading to Europe early in the month as prices rose toward one?month highs. Europe’s reliance on global LNG was exposed again when a major US winter storm disrupted American export capacity in late January. This storm—crucial because the US is Europe’s largest LNG provider—drove a sharp tightening in supply and contributed to European gas prices rising by more than 50% year?to?date as of 26 January. Domestic UK supply experienced its own pressure point when the Culzean gas field tripped on 12 January, temporarily reducing flows and adding upward support to prices. While Norwegian pipeline deliveries into the UK and northwest Europe were stable throughout the month, offering some relief, they were not sufficient to offset the broader decline in storage and the volatility in LNG availability.

Demand Factors

Demand conditions were equally shaped by shifting weather patterns. A series of Arctic outbreaks early and mid?month significantly increased heating demand across the UK and the continent, lifting gas futures and accelerating withdrawals from storage. However, this tightening was repeatedly countered by sudden shifts in meteorological outlooks, such as the milder forecast on 8 January and again on 19 January, each time causing markets to retrace earlier gains. Traders reacted strongly to every model update, particularly as both traditional and AI?driven forecasts struggled to track a persistent Siberian air mass that moved unpredictably across Europe. By the end of the month, forecasts again pointed towards further cold periods extending into early February, reinforcing expectations of firm demand and heightened market sensitivity. The global nature of the weather event—affecting Europe, Asia and the US—also intensified competition for LNG cargoes, especially as Asia prepared for its own cold spell, raising the risk that Europe could be outbid for marginal supply.

Geopolitical Factors

Geopolitical developments added further layers of uncertainty. Throughout the month, tensions involving Iran heightened the geopolitical risk premium, particularly because any escalation could disrupt LNG shipping routes through the Strait of Hormuz, a vital global chokepoint. These concerns were amplified on 29 January following renewed threats from the US administration towards Iran, which further supported gas price strength. Additionally, US–EU trade tensions flared mid?month, when new tariff threats raised fears of broader economic disruption. Although these threats primarily affected industrial demand expectations, they contributed to short?term volatility by influencing trader sentiment. Within the background commentary, the longer?term structural impact of losing Russian pipeline supply since 2022 was also evident.

Power Generation Factors

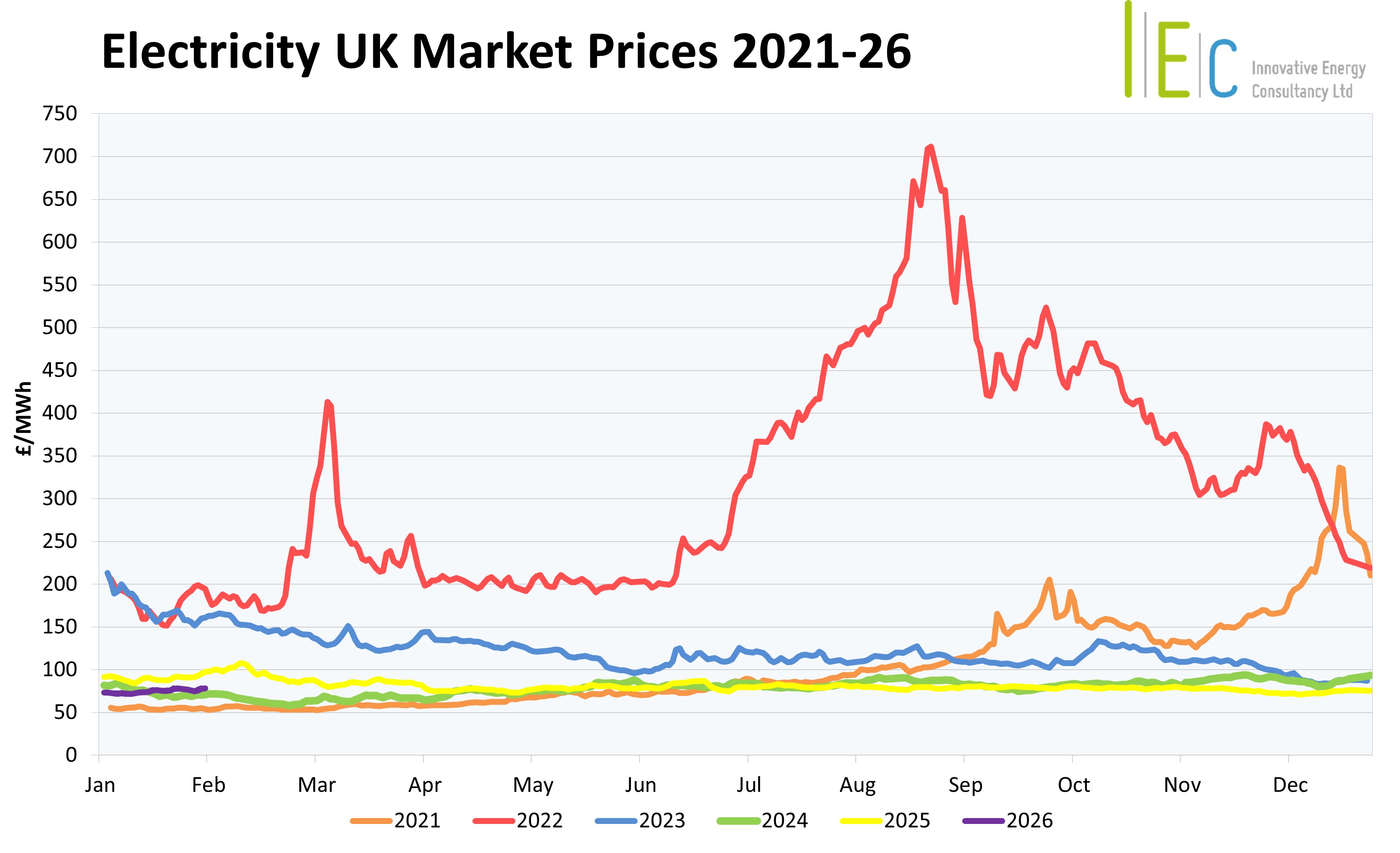

Britain’s power generation mix in January?2026 was shaped by strong renewable output and shifting winter weather patterns. Wind was the dominant source of electricity, delivering more than a third of total generation (37%) and significantly reducing reliance on gas during periods of higher wind speeds. Gas?fired power stations remained the second?largest contributor (31%) playing a crucial balancing role when colder, still conditions reduced renewable output. Alongside these major sources, electricity imports supported the grid during peak demand (11%), while nuclear output continued its gradual downward trend (10%). Biomass offered a steady share of dispatchable low?carbon generation (7%), and small contributions from solar, hydropower and battery storage added further system flexibility, reinforcing the growing role of zero?carbon sources in Britain’s electricity system. Major policy changes coming into force at end of 2025 saw the UK’s Emissions Trading Scheme (UKETS) price hike by 30%, peaking at £72/t mid-month before easing back to £64/t at the month-end.

We meet all your

business energy needs

Find out how much money

we’ve saved for our clients,

or to arrange an informal

discussion with one of

our energy experts,

please call 01244 571830